(Second of four-parts)

Last week, the Development Budget Coordination Committee (DBCC) or economic team kept the Philippine growth targets of 6-7% this year and 6.5-8% for 2024-2028, having considered the risks of El Niño, global trade tensions and value chain disruptions, among other factors.

Among their assumptions are inflation of 5-6% in 2023 and 2-4% in 2024-2028; peso-dollar rates of P54-P57 this year and P53-P57 in 2024-2028; Dubai crude at $70-$90 per barrel in 2023-2024 and $60-$80 in 2025-2028.

I think these growth targets are achievable and should be maintained. I can think of at least three reasons.

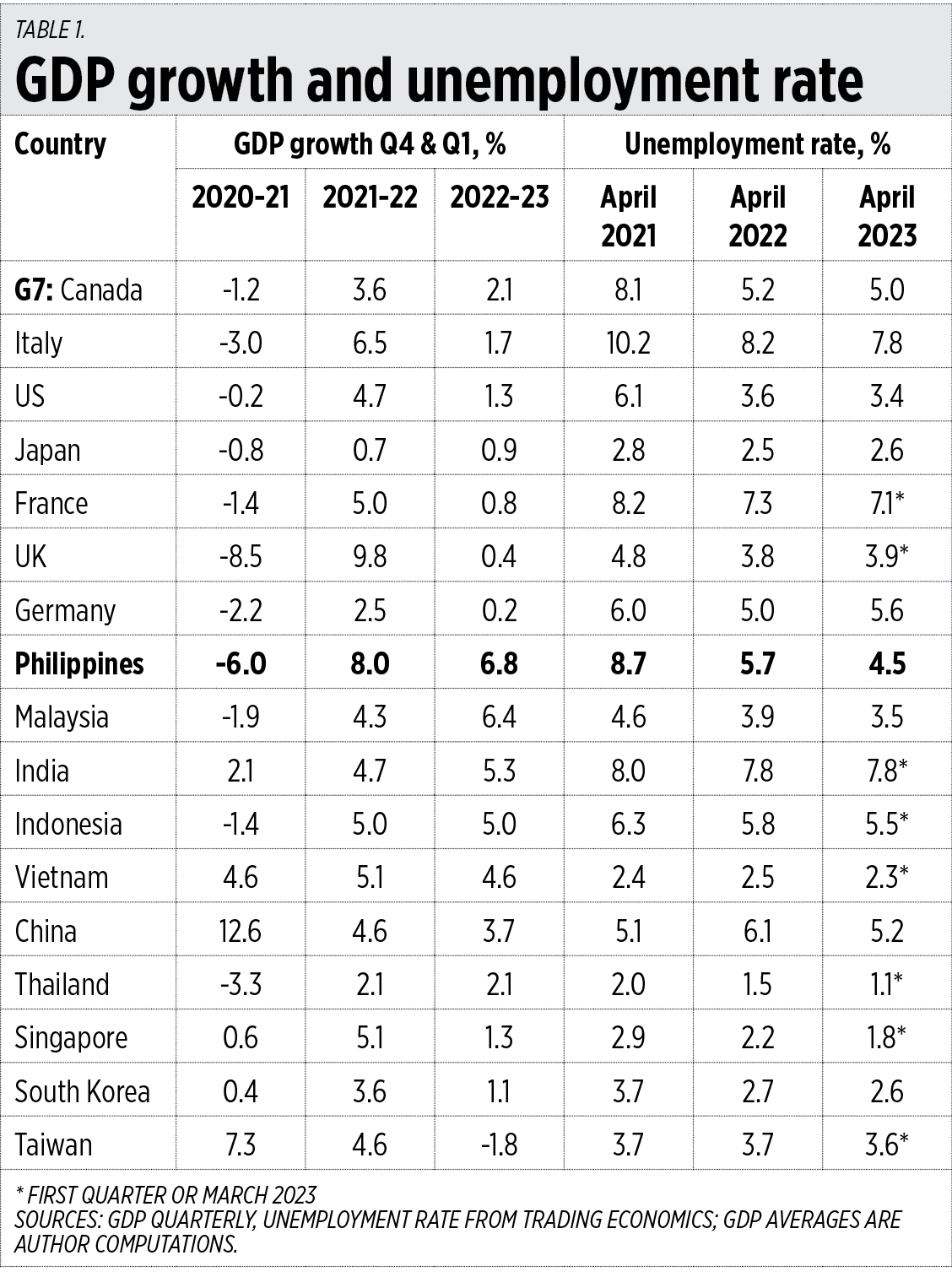

One, the Philippine growth momentum is way above the pace of neighboring Asian economies, and triple or quadruple those in G7 countries. Out of 72 economies that reported first quarter growth, the Philippines was the fifth-fastest growing and among the medium-to-large economies worldwide, the Philippines has the fastest growth.

Two, the average growth for the fourth quarter of 2022 and the first quarter this year was 6.8%, the fastest among the countries listed below, and it was a fast growth over a high base and high growth of 8% a year earlier.

Three, job creation remains fast as shown by the unemployment rate of 4.5% in April, which is almost one-half of 8.7% registered in April 2021 (Table 1).

{kind=link}

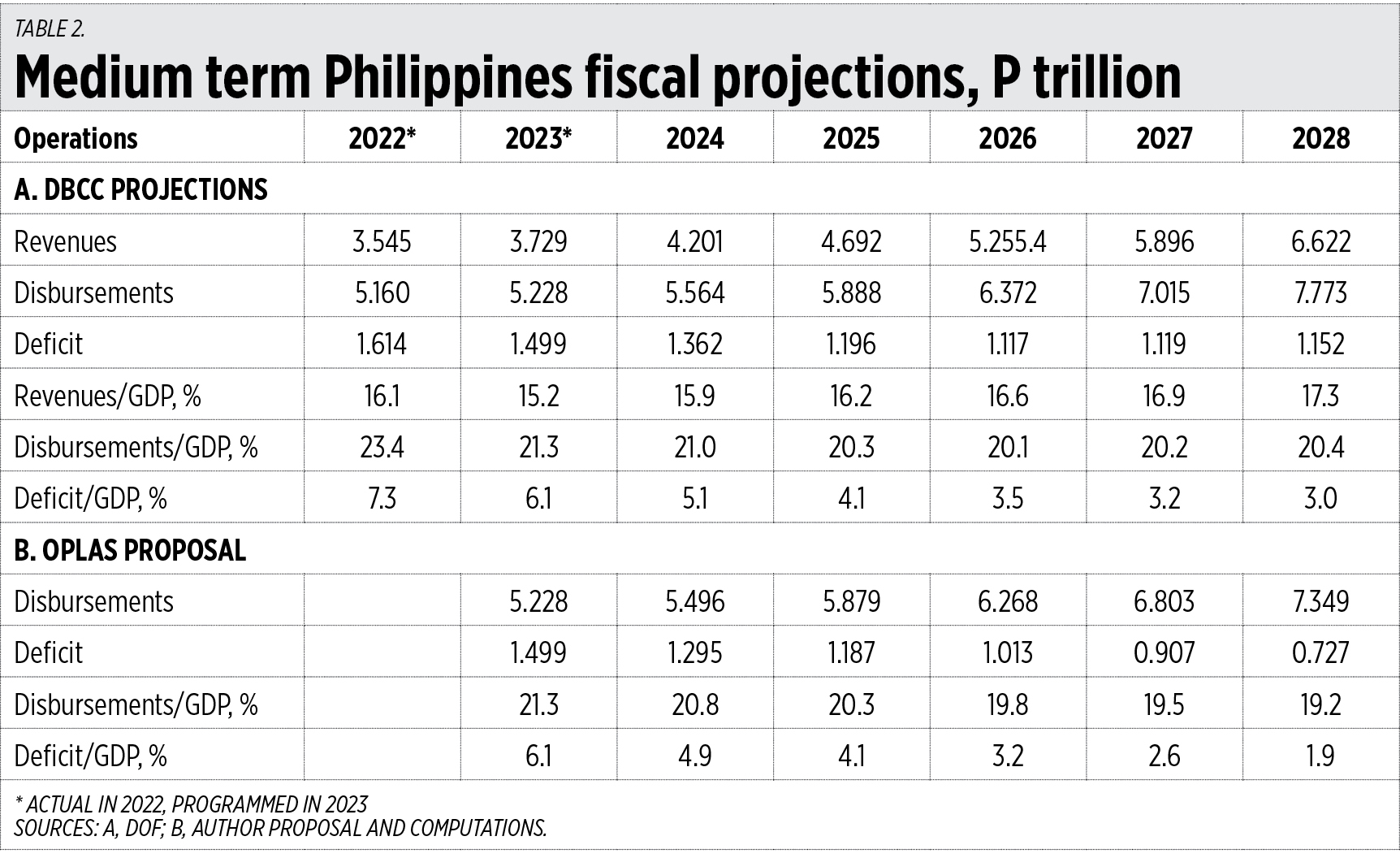

The DBCC also showed its medium-term fiscal scenario from 2023 to 2028. The revenue-to-GDP ratio will rise from 15.2% in 2023 to 17.3% in 2028, and the budget deficit-to-GDP ratio will decline from 6.1% in 2023 to 3% in 2028.

These are good targets by the DBCC, but we should aim for a drastic reduction in the annual budget deficit. This can be done via fiscal discipline — controlling spending and borrowings during noncrisis years, retiring public debt and saving on interest payments. When crisis years occur again, we will have wider fiscal leeway to engage in higher deficit spending and higher borrowings at lower interest.

Here, I propose that the disbursement-to-GDP ratio should decline from 21.3% this year to 20.3% in 2025 and 19.2% in 2028. Assuming that the revenue-to-GDP ratio will stay at DBCC targets, then the deficit-to-GDP ratio should significantly decline from 6% in 2023 to only 1.9% in 2028 (Table 2).

{kind=link}

Where can spending cuts be made? One in some subsidies and welfare programs. There are many subsidies and freebies that started many decades ago, including in healthcare and medicines, education from elementary to university, irrigation and agriculture credit, condoms and pills, monthly cash transfers, etc. Recently, food stamps were unveiled. New subsidies imply that some or many existing subsidies are hardly working. To finance new subsidies, some old subsidies must shrink or be stopped and rechanneled to new welfare programs.

Two, in National Government subsidies where there is high or rising subsidy programs by local government units (LGUs). LGUs now have more resources as a result of the Mandanas ruling, in which their share in national tax revenues have significantly increased.

Three, in big infrastructure projects via the Maharlika Investment Fund. Once the fund is established, many big projects that otherwise would be funded by taxes and public borrowings can be taken by the fund.

These include inter-island bridges (Panay-Guimaras-Negros bridge, new Samar-Leyte bridge, Cavite-Corregidor-Bataan bridge, etc.); small modular reactors for off-grid islands and provinces to stop endless subsidies to National Power Corp. gensets. We can also revive the Bataan Nuclear Power Plant, which has potential generation (assuming a capacity factor of 85%) of 4.62 million megawatt-hours yearly, much larger than solar and wind’s combined generation of 2.71 million MWh in 2021, and reduce electricity prices. The plant was killed in 1986 due to politics. Even business conglomerates would be hesitant to revive this plant because of heavy politics in the energy and environment sectors.

The Philippines has big metallic mining potentials especially for gold, copper and nickel. The Maharlika fund should go there and generate more jobs, more forex revenues and pay more mining taxes. The single-biggest foreign direct investment for the Philippines would have been the $5.9-billion Tampakan gold-copper project by Sagittarius Mines in South Cotabato. The provincial government simply disallowed open-pit mining and the project failed to take off.

Potential projects like these may have failed to register in the minds of the authors of “Maharlika Investment Fund: Still Beyond Repair,” a 27-page paper written by faculty members of my alma mater, the UP School of Economics. Among the reasons they oppose the fund are the inability to articulate implications of the fund’s dual-bottom line objective, funding the MIF poses huge risks to strained public coffers and is vulnerable to moral hazard, and the unlikely ability to crowd in investments and eke out large returns.

Several government agencies are ironically the hurdles and disruptors of important infrastructure and energy projects. If the Maharlika fund is involved in reviving the Bataan plant and in big mining projects, local governments and national bureaucracies can’t easily delay or stop the operation of these big projects knowing there is National Government involvement. Thus, these objections are addressed. The second objection is also addressed as big private capital comes in.

If the fund is questioned or opposed, my question is why Malampaya royalties, which averaged P23 billion a year from 2018 to 2022, were not included in the funding.

The Philippines should endlessly push for fast economic growth. Financing and sustaining it via rechanneled public resources from nonworking subsidy programs, plus government resources outside taxes and borrowings like the Maharlika fund, are noteworthy initiatives.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers