(Part 1 of 4)

The Ferdinand Marcos, Jr. administration turned one year old last week on June 30. This column will produce a four-part assessment of the economic performance of the Marcos Jr. administration leading to the second State of the Nation Address (SONA) on July 24.

The goal of this informal exercise is to assess if the first year performance so far would help the Philippines achieve fast growth — create more jobs, expand the production of more goods and services, further industrialize and modernize the Philippines in the medium- to long-term.

Eight economic sectors, two per article, will be assessed this month: the budget deficit, unemployment, inflation, the interest rate, GDP growth, agriculture, trade, and investment.

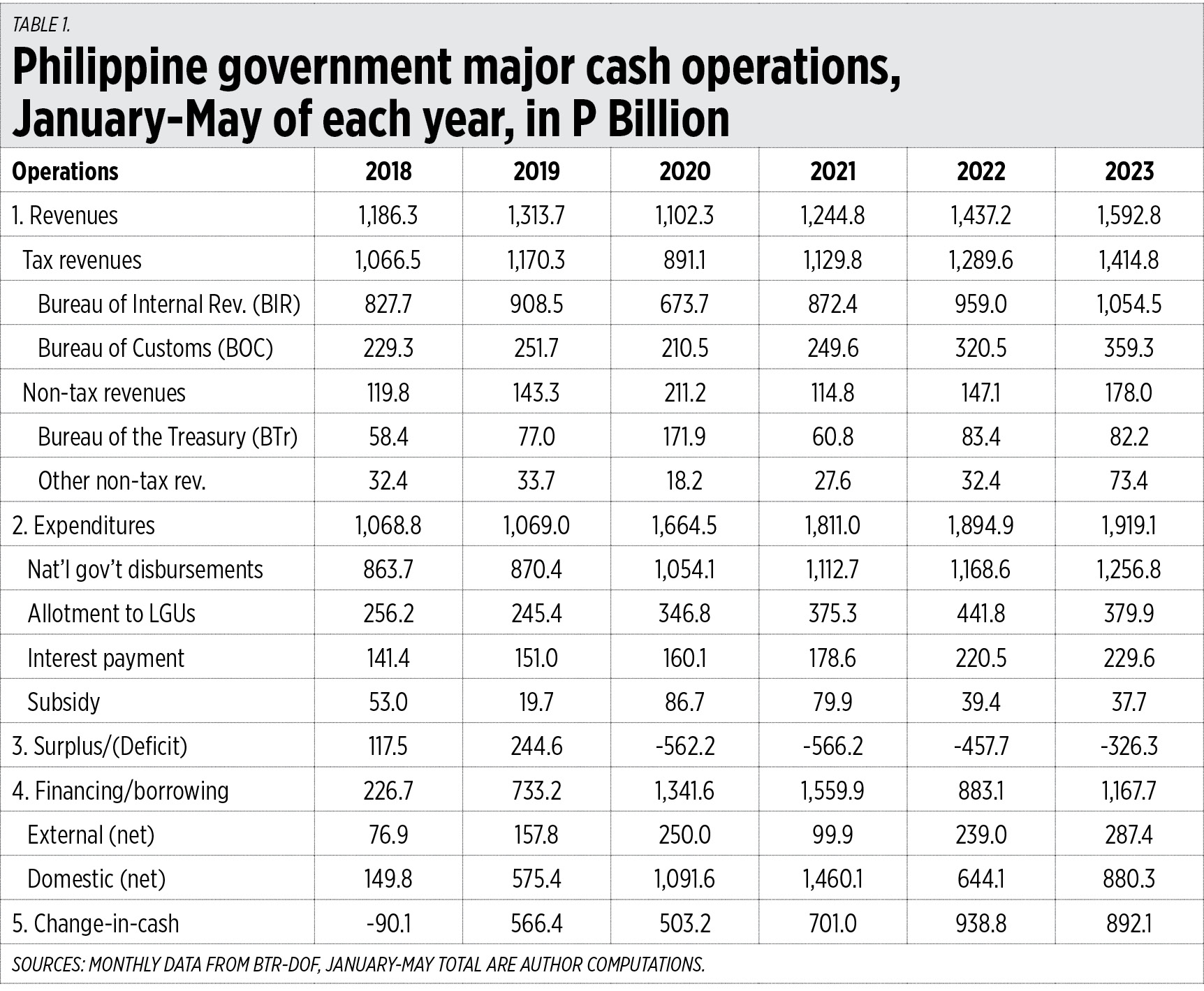

CASH OPERATIONS REPORTLast week, the Bureau of the Treasury (BTr) released the cash operations report for May 2023. The January-May 2023 data are available, so I will compare the numbers with performance in the same months of 2018 to 2022. The results are generally good.

One, revenues this year have significantly improved, reaching P1.59 trillion from P1.44 trillion last year. This is important for two reasons: there was no tax hike, and lockdown-era tax cuts still remained in place. So, an improvement in economic activities, not a tax hike, expanded the tax base.

Two, expenditures have mildly increased to P1.92 trillion this year from P1.89 trillion last year. While allocations for local government units have declined this year, National Government disbursement remains high as there is spending that continues to remain bloated like the military and uniformed personnel (MUP) pension. This fund must decline significantly if we must control the annual deficit, financing, and borrowing.

Three, the budget deficit has declined to only P326 billion this year from an average of P529 billion/year in the last three years 2020-2022, so this is good news. Financing or borrowing has mellowed to P1.17 trillion this year, higher than 2022 but lower than in 2020 and 2021 (see Table 1).

{kind=link}

Interest payment is high, already P230 billion in the first five months of 2023 alone. This is a reflection of the huge increase in public debt during the lockdown years of 2020-2021 and this is not good. We should aim to reduce the annual budget deficit, reduce the need for borrowing, find new revenues like the large privatization of some government assets, in order to retire more public debt while controlling the rise in spending.

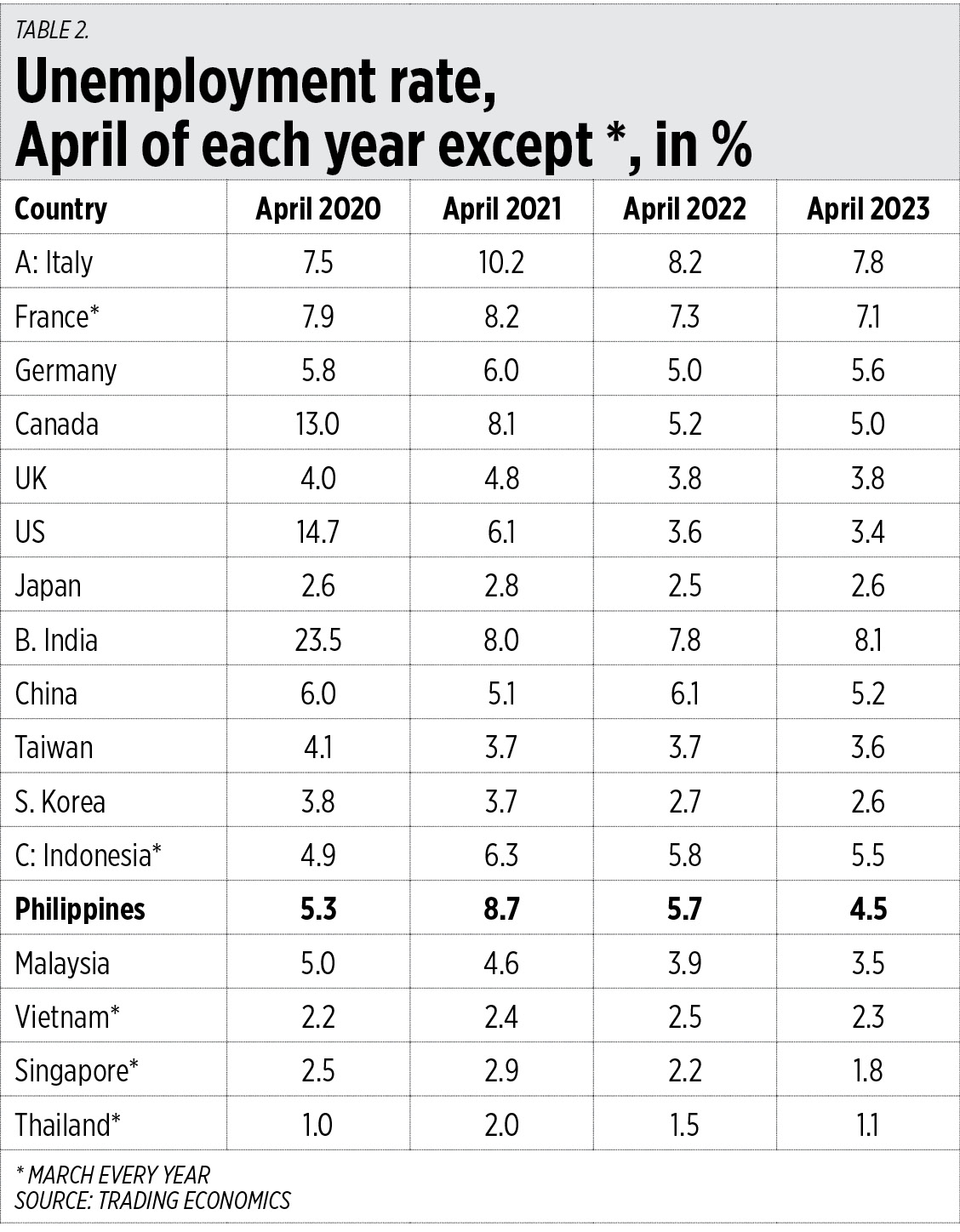

DECLINING UNEMPLOYMENTNext is the labor market. In Table 2, I group countries into three: group A are G7 member countries, group B are the big North and South Asian economies, and group C are the ASEAN-6 or the six large economies of the regional bloc.

{kind=link}

As of April 2023, four of the G7 countries, plus India and China, and Indonesia in the ASEAN-6 countries had unemployment rates of 5% and above of the labor force. The Philippines’ unemployment rate has significantly declined to only 4.5% which is almost half the 8.7% registered in April 2021, so this is good news.

More Filipinos now have jobs and, hence, have money to spend and buy, which will create more consumer demand and invite more business expansion and innovation.

So far, considering these two indicators — budget deficit and unemployment rate — the Philippines under the Marcos Jr. administration is doing well. These are consistent with the economic team’s high growth target of 6-7% in 2023 and 6.5-8% in 2024-2028. Meaning if both the deficit and unemployment rate continue their downward trends, the high growth targets are achievable, and, better yet, may be surpassed.

We should target high employment, high productivity, and high economic ambition. Go for high revenues and high investments, and a low deficit and low borrowings. Aim for becoming an upper middle-income country — with a per capita income of $4,046 to $12,535 per year — by 2028 or earlier, vs. the current level of $3,623 in 2022.

This is achievable if we have a single-track goal: more growth, expanded production, more economic and business competition. Aim for a larger economic pie, not “well-distributed” shares in a small economic pie.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers.