By Keisha B. Ta-asan, Reporter

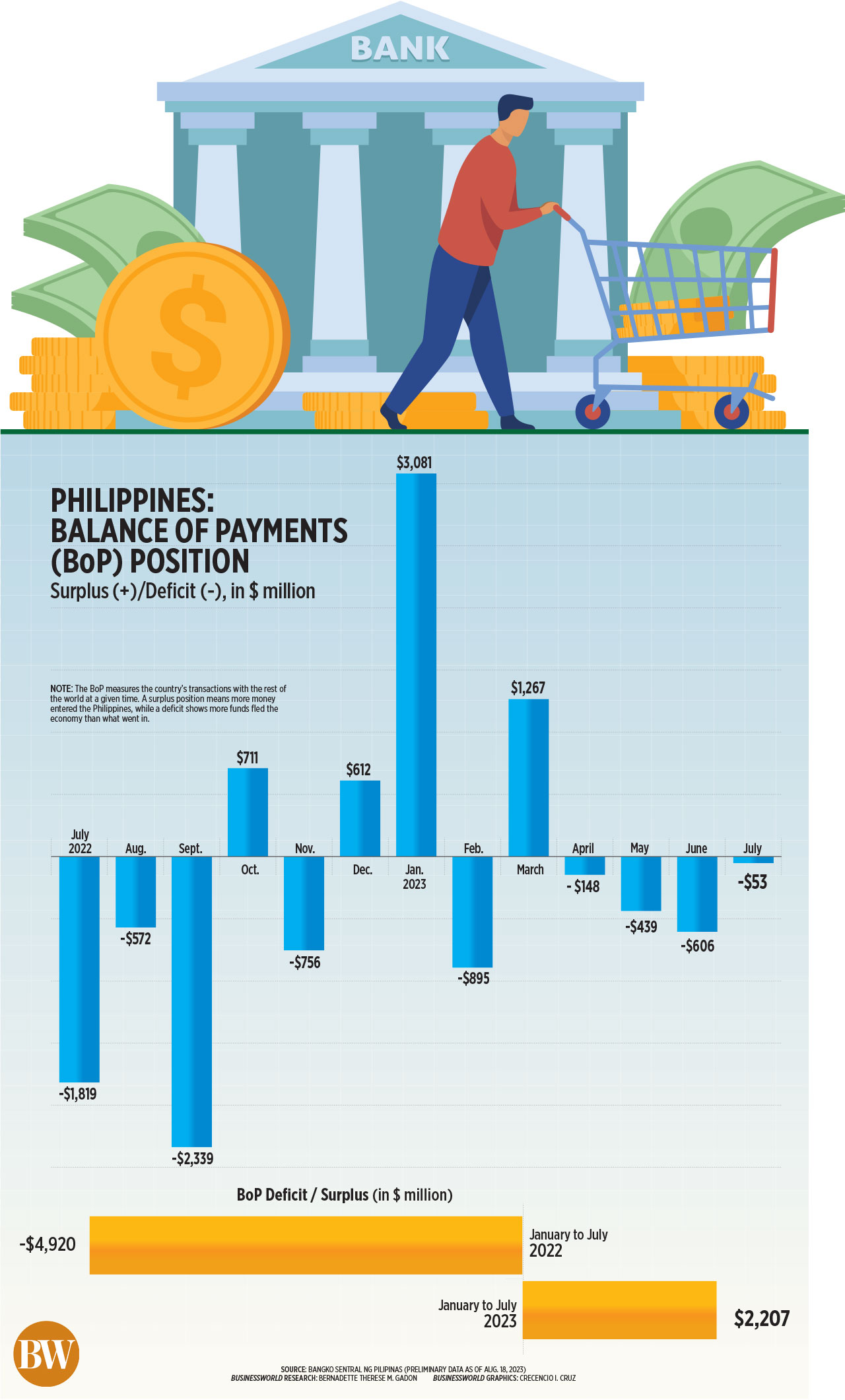

THE OVERALL balance of payments (BoP) deficit sharply narrowed to $53 million in July, as more dollars flowed out of the country to pay for the government’s foreign debt.

The BoP shortfall in July was significantly smaller than the $1.8-billion gap in the same month a year ago and $606 million in June, data released by the Bangko Sentral ng Pilipinas (BSP) late on Friday showed.

This is the narrowest BoP deficit in three months or since the $148-million gap in April.

July also marked the fourth straight month the BoP position was in a deficit.

{kind=link}

“The BoP deficit in July 2023 reflected net outflows arising mainly from the National Government’s (NG) payments of its foreign currency debt obligations,” the BSP said in a statement.

The BoP measures the country’s transactions with the rest of the world at a given time. A deficit means more funds fled the economy than what went in, while a surplus shows that more money entered the Philippines.

In the first seven months of the year, the BoP position swung to a surplus of $2.21 billion, from the $4.92-billion deficit in the same period in 2022.

“Based on preliminary data, this development reflected mainly the improvement in the balance of trade and the sustained inflows from personal remittances, net foreign borrowings by the NG, trade in services, and foreign direct investments,” the BSP said.

Rizal Commercial Banking Corp. Chief Economist Michael L. Ricafort said the smaller BoP deficit in July is likely due to the narrowing of the country’s trade deficit.

The trade deficit for January-June reached $27.96 billion, slightly narrowing from the $29.8-billion deficit posted in the same period last year.

Mr. Ricafort said the narrower BoP deficit was also due to the continued growth in dollar inflows from remittances, business process outsourcing revenues, foreign tourism receipts, profit from Philippine Offshore Gaming Operators (POGO) firms and foreign investments.

The central bank also noted the BoP position reflects the final gross international reserves (GIR) level of $100 billion as of end-July, 0.6% higher than the $99.4 billion as of end-June.

The GIR level reflects a more than adequate liquidity buffer equal to 7.4 months’ worth of imports of goods and payments of services and primary income.

“Specifically, it ensures availability of foreign exchange to meet balance of payments financing needs, such as for payment of imports and debt service, in extreme conditions when there are no export earnings or foreign loans,” the BSP said.

The GIR can also cover up to 5.9 times the country’s short-term external debt based on original maturity and 4.1 times based on residual maturity.

Further growth in dollar inflows and continued narrowing of the country’s trade deficit will support the BoP position of the Philippines moving forward, Mr. Ricafort said.

The planned retail dollar bond offering by the National Government as well as its debut of about $1-billion Islamic bonds this year will boost the dollar reserves, he said.

The government is eyeing to launch a retail dollar bond offering in the third quarter, with an offer size of around $2 billion. The last retail dollar bond sale was in 2021, when the Philippines raised almost $1.6 billion or P80.91 billion.

Earlier in June, the central bank revised its BoP deficit forecast to $1.2 billion or equivalent to -0.3% of gross domestic product (GDP), down from the $1.6-billion (-1.3% of GDP) forecast in March.

The BSP also projected a narrower current account deficit at $15.1 billion (-3.4% of GDP) this year from $17.1 billion (-4% of GDP) previously.

The country’s GIR is expected to hit $100 billion by end-2022 and $102 billion by end-2023.