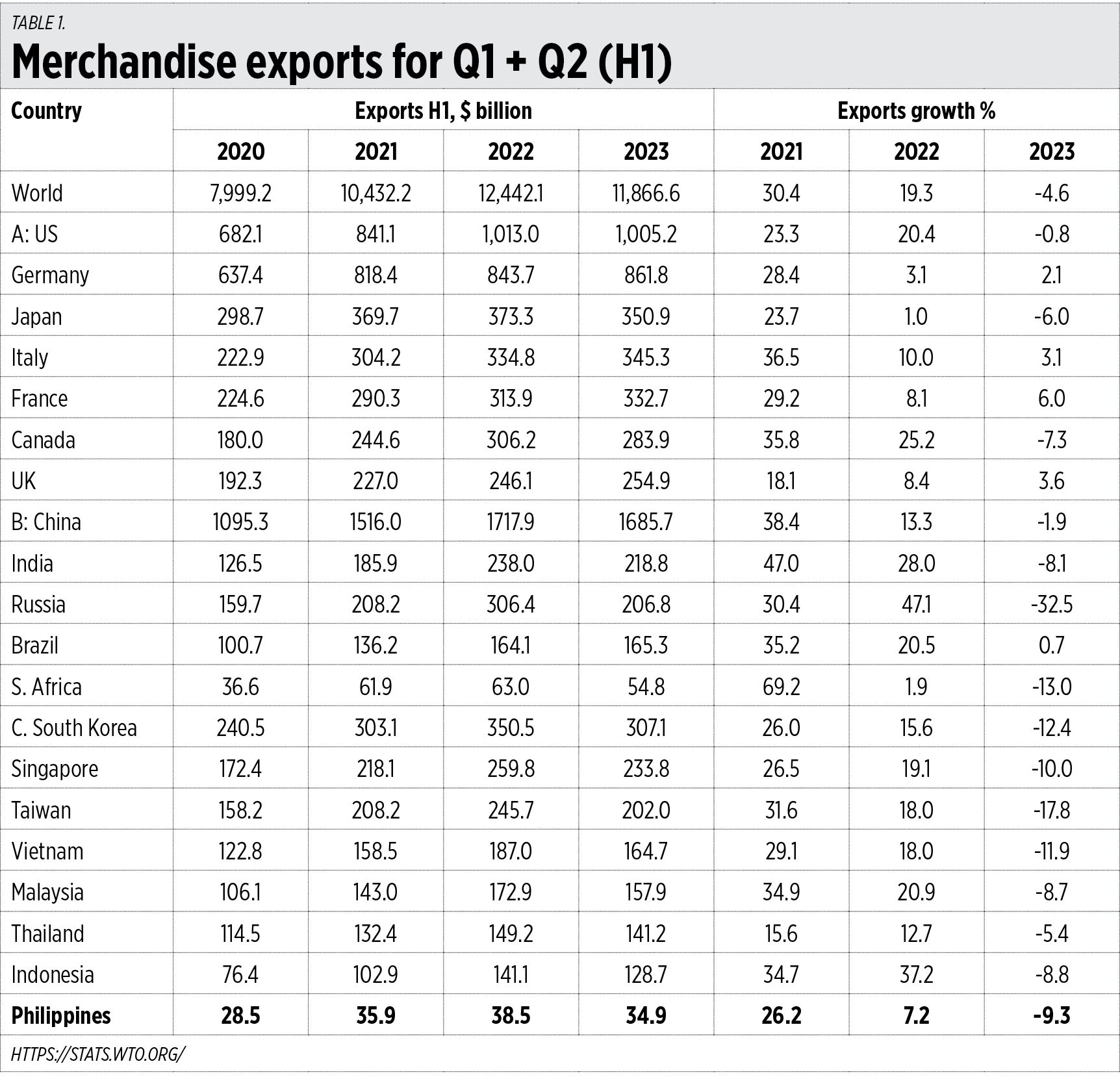

The deteriorating global and regional economic environment this year is better seen in the deceleration in value and growth of merchandise trade. The World Trade Organization (WTO) has reported the second quarter (Q2) 2023 data for merchandise exports.

In Table 1, I compare exports performance in Q1 + Q2 or the first half (H1) of 2020 to 2023. Global exports contracted by 4.6% in H1 2023 compared to H1 2022. I grouped the countries into three: Group A is made up of G7 industrial countries, Group B is the BRICS nations, and Group C contains major and medium East Asian exporters. European exports have expanded among each other, but all East Asian exporting countries plus India suffered contractions this year.

{kind=link}

Despite this trend, the fastest growing major economies in the world are Asian, led by India, China, the Philippines, and Indonesia with gross domestic product (GDP) growth of 5% to 7% in H1 2023, whereas Europeans were crawling at -0.2% to 1.2% over the same period.

I think the main explanation for this is the dynamic domestic economies of these four Asian countries thanks to their big populations: 1.4 billion each for China and India, and 275 million and 113 million for Indonesia and the Philippines, respectively. The beauty of having a big population is it also means there is a big supply of entrepreneurs and workers, producers and consumers. So, when the global business and economic environment deteriorates, there is a big and strong domestic market to continue the business momentum.

Nonetheless, Philippines merchandise exports were the smallest among the ASEAN-6. There is a need to clear up bottlenecks in exports production and trade facilitation. See the BusinessWorld reports related to this, written by Justine Irish D. Tabile and John Victor D. Ordoñez: “Five ecozones could be proclaimed by October” (Sept. 17), “Trade boost expected from partnerships forged by ASEAN business organizations” (Sept. 19), “PCCI to help encourage greater use of FTAs” (Sept. 25), and, “PPP bill approved on 3rd reading” (Sept. 25).

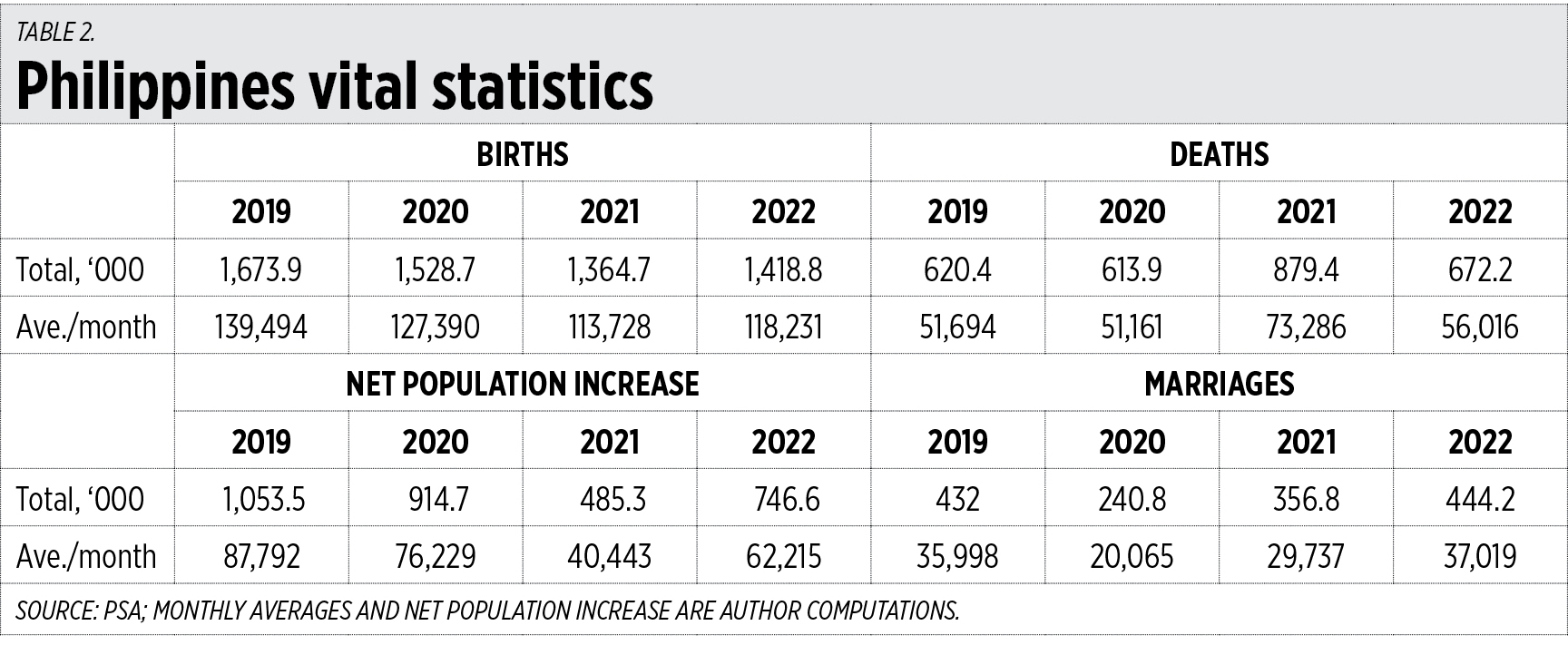

Back to population and economic growth. In the middle of this month, the Philippine Statistics Authority (PSA) released 2022’s full monthly data for vital statistics. I summarize the annual and average monthly data (see Table 2).

{kind=link}

Births: There was consistent decline in the number of births, from 139,500/month in 2019 to only 113,700/month in 2021 which is bad. The good thing was that there was a slight recovery to 118,200/month in 2022, but it is still low compared to 2019’s average.

Deaths: There was no excess mortality in 2020 compared to 2019 despite all the scare mongering over COVID-19 and its related severe lockdowns and business closures. High excess mortality occurred in 2021 — nearly 22,000/month over 2019 levels — especially in the second half when mass vaccination went full blast.

The computed net increase in population (births less deaths) has declined from 87,800/month in 2019 to only 40,400/month in 2021, and slightly up to 62,200/month in 2022.

Marriages have declined significantly, from 36,000/month in 2019 to only 20,000/month in 2020. This has recovered to 37,000/month in 2022 (see Table 2).

There is a need to relax the implementation of the Reproductive Health (RH) law of 2012 (RA 10354). State funding of population control-leaning programs is wrong.

There is also a need to review and assess the impact of mass vaccination against COVID on human fertility, both short and long-term.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers