“And so this is Christmas, For weak and for strong/The rich and the poor ones, The road is so long/And so happy Christmas, For black and for white/For yellow and red ones, Let’s stop all the fight.”

— John Lennon, “Happy Christmas (war is over),” 1971.

“There’s so many different worlds, So many different suns/And we have just one world, But we live in different ones/Now the sun’s gone to hell and, The moon’s riding high/Let me bid you farewell, Every man has to die/But it’s written in the starlight, And every line in your palm/We’re fools to make war, On our brothers in arms.”

— Mark Knopfler/Dire Straits, “Brothers in Arms,” 1985.

ADVANCED Merry Christmas, dear readers. Those words above from two of my many rock idols occasionally hum in my head when I read and hear about the ongoing brutal wars in Europe and the Middle East, and there are hints of the wars ending soon. And I hope it will be by the first quarter of 2024.

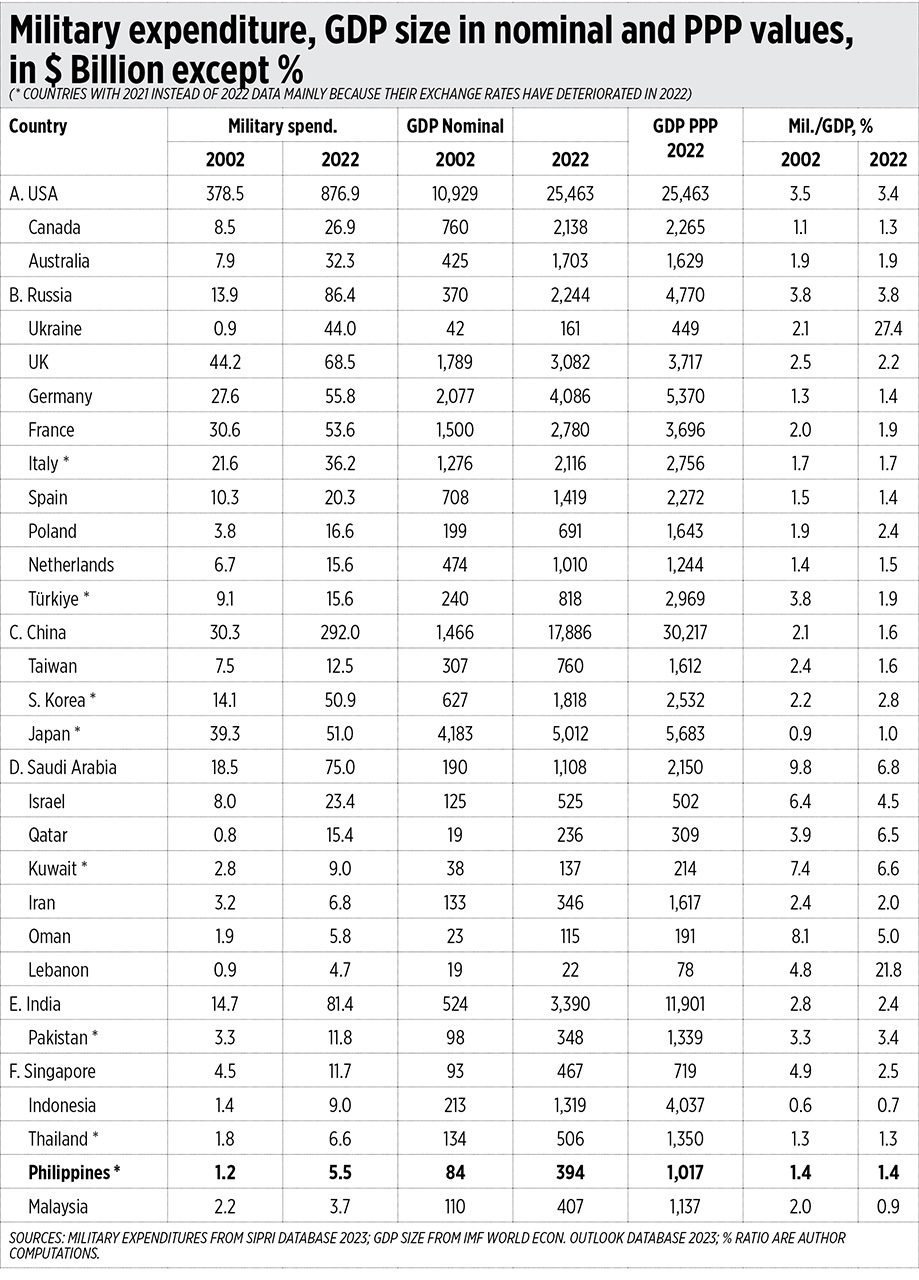

For this column I constructed a table showing how much countries spend on armaments and other military spending, and I compared the spending data with their GDP size. The source of data on military expenditure is the Stockholm International Peace Research Institute (SIPRI).

I grouped the countries into six. In Group A are the US, Canada, and Australia which can join any war in the Atlantic and Pacific sides, with Australia more focused on the Pacific. In Group B are countries involved in the Russia-Ukraine war. In Group C are those involved in the potential conflicts between China and Taiwan and North and South Korea. Those in Group D are involved directly or indirectly in the Israel-Gaza/Hamas war. In Group E are India and Pakistan which have a big territorial conflict over Kashmir. And in Group F are the ASEAN-5, which are not directly involved in any of the above-mentioned conflicts. Other countries which are involved in any of those regional conflicts but whose military spending is below $4 billion were not included in the table for the purpose of brevity.

Here are 10 trends in the economics of war, and our path to global peace.

One, the economics of war is that for some countries, “war is business” and hence, more actual wars or war preparations mean more business. This applies largely to countries like the US (think of its companies like Lockheed, Raytheon, Boeing, Northrop, General Dynamics…), the UK (BAE), and China (Norinco, AVIC…).

Two, these major arms exporting countries are often also those with high oil-gas demands yet have limited oil-gas production and reserves. Hence, a lot of past and current wars are in the Middle East (the US invasion of Iraq, a big portion of Syria), plus Russia which has huge oil-gas-coal reserves. The presence of a non-Muslim Israel in the Middle East neighboring Palestine is, of course, a big factor for the endless instability in the region.

Three, the US has the largest military expenditure in the whole world at $877 billion in 2022, three times larger than China’s $292 billion, and 10.2 times larger than Russia’s $86 billion. The US’ military spending/GDP ratio remains flat at 3.5% for the two decades from 2002 to 2022.

Four, Europe’s top five largest countries outside Russia (the UK, Germany, France, Italy, Spain) alone have combined military expenditures of $231.7 billion in 2022, which is 2.7 times larger than Russia’s. Ukraine military spending jumped from $1 billion in 2002 to $44 billion in 2022, much of its money and armaments sent by the US and NATO countries.

Five, Russia is not China. The Russian economy is “small” compared to China’s, its GDP nominal size of $2.2 trillion in 2022 is only 1/8th of China’s $17.9 trillion. And Russia’s military spending is only a third of China’s. If the US plus other big NATO countries cannot defeat Russia in their proxy war via Ukraine, there is big question mark over if the US and NATO can defeat China over the Taiwan issue.

Six, countries with the largest military spending/GDP ratio are not in NATO but in the Middle East. Saudi Arabia, Qatar, Kuwait, and possibly the United Arab Emirates (there is no data for 2021 or 2022) have 6-7% of GDP. But Iran, considering western media’s exaggeration that it has huge military spending, actually has a small ratio of only 2%. In contrast, poor Lebanon, with a GDP of only $22 billion in 2022 (smaller than Cambodia’s $29 billion and slightly larger than Brunei’s $17 billion) has military spending of 22% of GDP. Really weird and wasteful.

Seven, India, with its territorial conflict with Pakistan over Kashmir, also has a territorial conflict with China and hence is ramping up its defense spending. But its military/GDP ratio remains modest at 2.4%.

Eight, ASEAN countries with generally fast GDP growth continue to have modest military spending compared to many countries and regions in the world and this is good. Only Singapore has a military/GDP ratio of larger than 1.5% (see the table).

{kind=link}

Nine, the so-called “rules based international order” (RBIR) is double talk. Invasion is wrong and anti-RBIR if the invader is Russia (invading Ukraine) or China (possibly invading Taiwan). But invasion is justified and consistent with RBIR if the invader is the US and other western NATO countries (see Vietnam, Afghanistan, Iraq, Syria, etc.). Invasion is invasion and we should condemn it whether the invader is Russia or America or China. We should focus on non-interference, stop these endless wars, stop regime-change via external aggression.

Ten, countries and humanity should focus on global peace and prosperity, diplomacy and wealth creation, not heavy armaments procurement and military destruction. We should devote our manpower to commerce, tourism, and investment and not on training so many soldiers and gun-toting warriors. Let John Lennon and Mark Knopfler’s words prevail in international politics and economics.

Hoping for peace and prosperity, hoping for an end to the Ukraine war and the Middle East war by early 2024. And hoping for no war whatsoever over Taiwan, over disputed atolls in the South China Sea or West Philippine Sea.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.