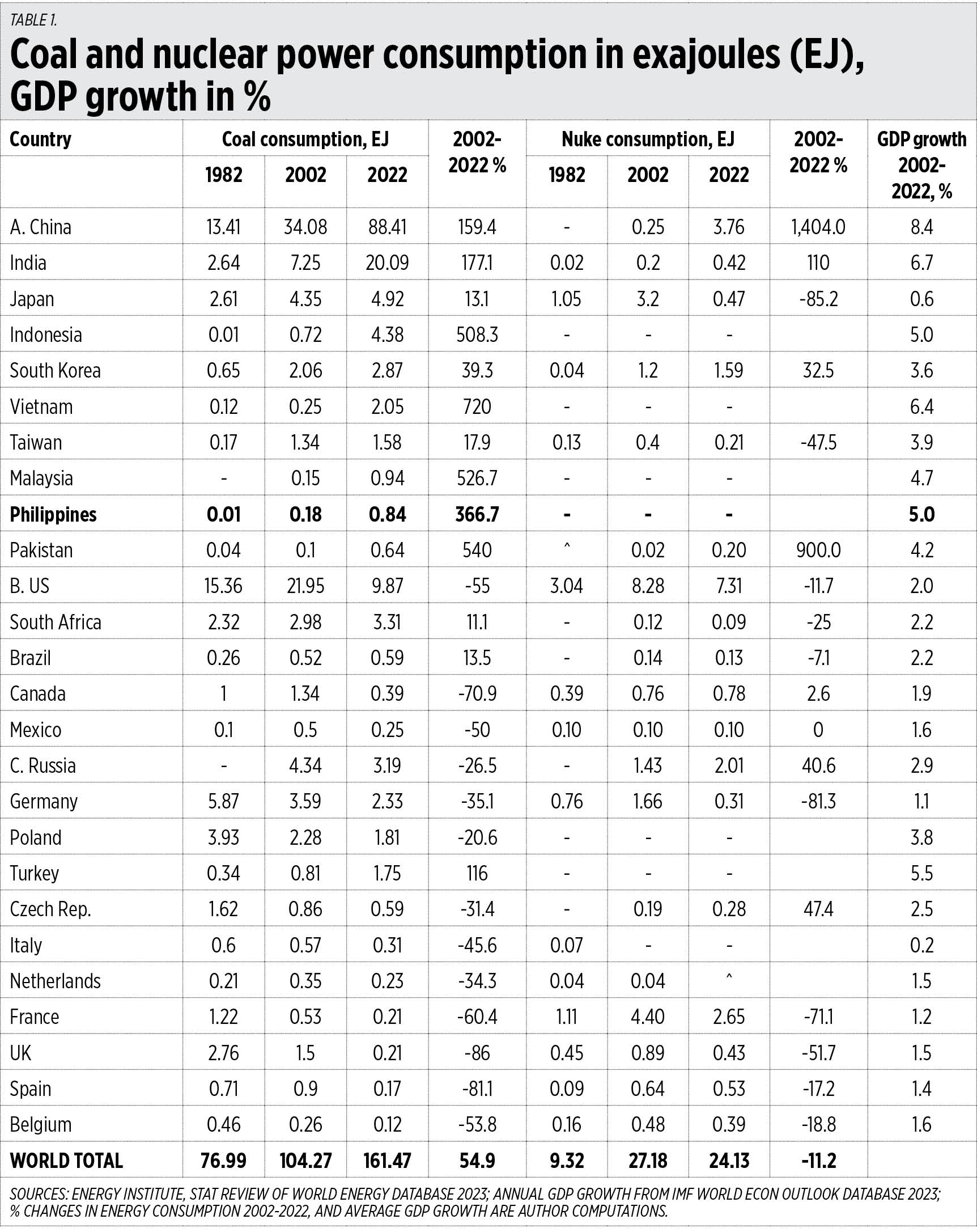

Happy New Year, dear readers. Here’s a lookback of important developments in the global energy industry. In the table below, I grouped the countries into three — group for Asia, group B for the Americas plus South Africa and group C for Europe.

First, “decarbonization” and coal phasedown continued in Europe and developed economies in North America and Asia, while developing Asia added more coal capacity and consumption. Global coal consumption from 2002-2022 expanded by 55%.

Second, “denuclearization” of the power system also continued in Europe. Germany shut down all its remaining nuclear power plants in April; France had targeted to cut its nuclear power share to 50% from 75% of the total by 2035, but was forced to abandon the goal; Spain announced a nuclear phaseout by 2035. In Asia, only Japan and Taiwan have joined this trend. Global nuclear consumption in the past two decades declined by 11%.

Third, slow, anemic economic growth continued to plague “decarbonizing” Europe in the past two decades, and some countries there likely to have contracted in 2023 (Germany, Poland, Ireland, etc.). “Carbonizing” Asians that need cheap, stable energy sources keep humming with high growth except Japan (Table 1).

{kind=link}

Fourth, all the gloom and doom scenarios in oil prices because of the continuing war between Russia and Ukraine plus NATO, and even with the war between Israel and Hamas plus Hezbollah and Houthis since early October 2023 did not happen. WTI crude price ended 2023 at below $73/barrel while it was $90 days before the Russian invasion in late February 2022.

Fifth, it’s the same trend for gas and coal. The end-2023 US natural gas price of about $2.5/mmbtu was much lower than $4.5/mmbtu in mid-February 2022 before the Ukraine war. The end-2023 coal (Newcastle) price of about $146/ton is again much lower than the pre-Ukraine war price of $240/ton.

Sixth, both the solar energy index and wind energy index are below $300, the lowest since October 2020. The EU carbon permits are below $85/ton, another low level since December 2021. In contrast, the nuclear energy index reached an all-time high of $2,007 in December.

Seventh, the biggest annual UN meeting, Conference of Parties (COP) 28 in Dubai from Nov. 30 to Dec. 12 attracted more than 70,000 foreign participants including media, activists and billionaires who lambasted fossil fuels while using lots of it flying from around the world to Dubai. The key agreement was not the phaseout of fossil fuels but the transition away from fossil fuels.

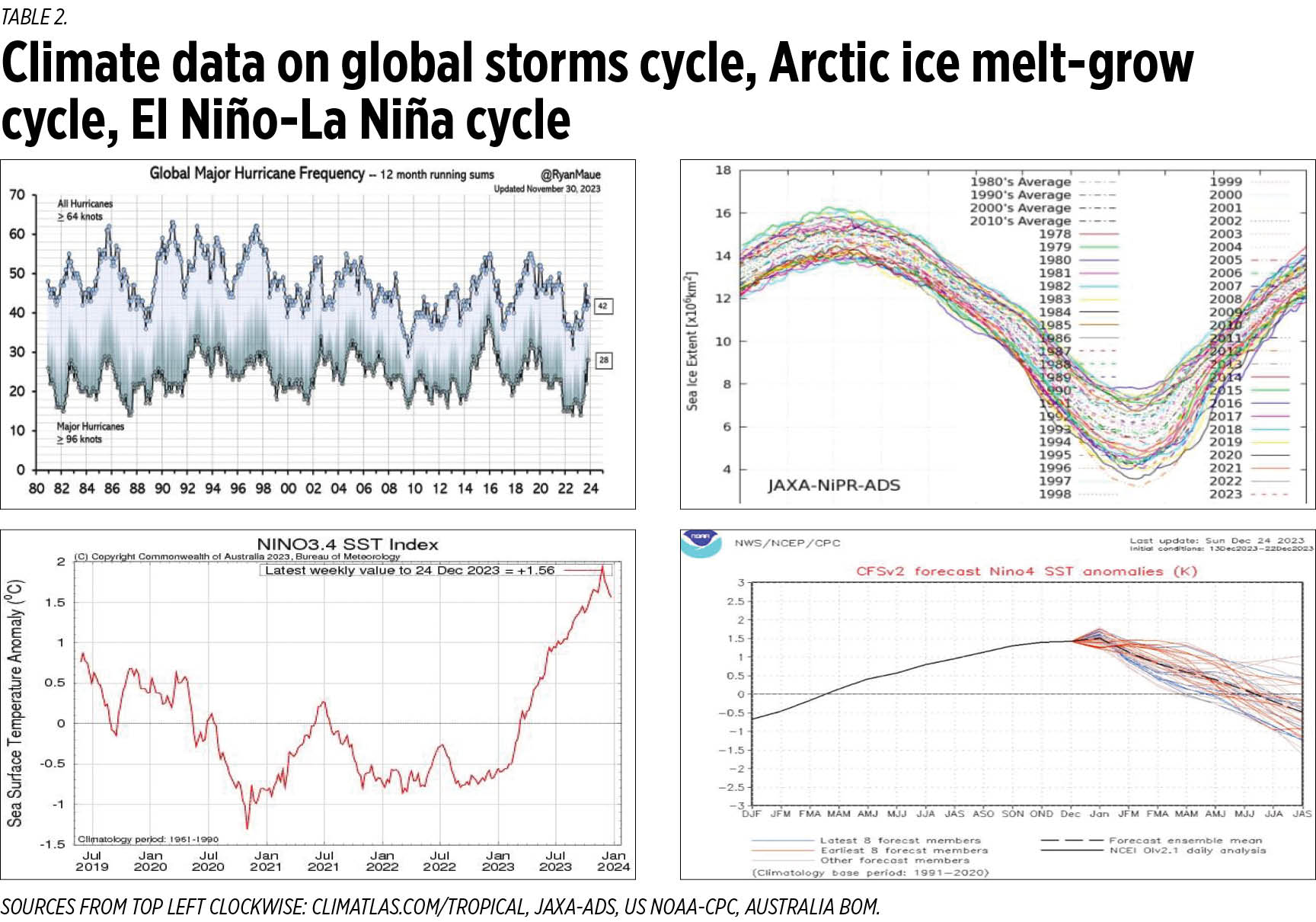

Eighth, the gloom and doom climate scenarios of the ever-warming, ice-melting and sea level-rising planet, more and stronger storms, did not happen, as shown by the two charts below from the Japan Aerospace Exploration Agency (JAXA) Arctic and Antarctica Data archive System (ADS), and climatlas.com/tropical by Ryan Maue. The JAXA-ADS data from 1978 to December 2023 showed ice-melt growing each year, or a 100% natural cycle. Arctic ice is lowest in September each year with only about 4 million sq. km, then the ice starts growing to the highest in March each year with up to 16 million sq. km of ice. For context, the total land area of the Philippines is only 0.3 million sq. km; the lowest level Arctic ice is 13x larger, and the highest level Arctic ice is 53x larger than the total land area of the Philippines.

Ninth, the “scary droughty” El Niño of 2023 showed a fast rise in ocean temperatures, but was quickly followed by a fast decline in temperatures. This occurred after a triple-dip La Niña. Two lower charts below are from the Australia Bureau of Meteorology (BoM) and US National Oceanic and Atmospheric Administration (NOAA) Climate Prediction Center (CPC). The BoM data from May 2019 to Dec. 24, 2023 showed that the triple-dip La Niña and global cooling occurred from July 2019 to March 2021. Triple-dip La Niña is rare, and the last time it happened was 21 years ago. The NOAA-CPC data as of Dec. 24, 2023 showed that the current El Niño would end by May 2024, go to a neutral stage and go back to La Niña by September 2024 (Table 2).

{kind=link}

Tenth, Uranium prices are at an all-time high. From the end-December 2021 price of only $44/lb, it went up to $49/lb by end-December 2022. During the COP28 meeting, it was up to $82. A week after COP28 ended, it went up to $86, and two weeks after it further rose to $91. It seems that the COP resolution of the “transition away from fossil fuels” means countries and companies will start investing in nuclear power, and not in intermittent wind-solar.

Philippines economic and energy policies should focus on sustaining fast growth to help create more jobs and attract more businesses. A number of big companies from Germany, the UK, Italy, etc. have either moved to other countries partly due to expensive energy in their home countries. The Philippines should attract more foreign companies and professionals by not following the folly of “decarbonization” and “net zero” fetishism and obsession.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.