THE PHILIPPINE Statistics Authority (PSA) released the fourth quarter (Q4) 2023 GDP data yesterday — it showed that GDP grew by 5.6%. Full year 2023 growth was also 5.6% — good.

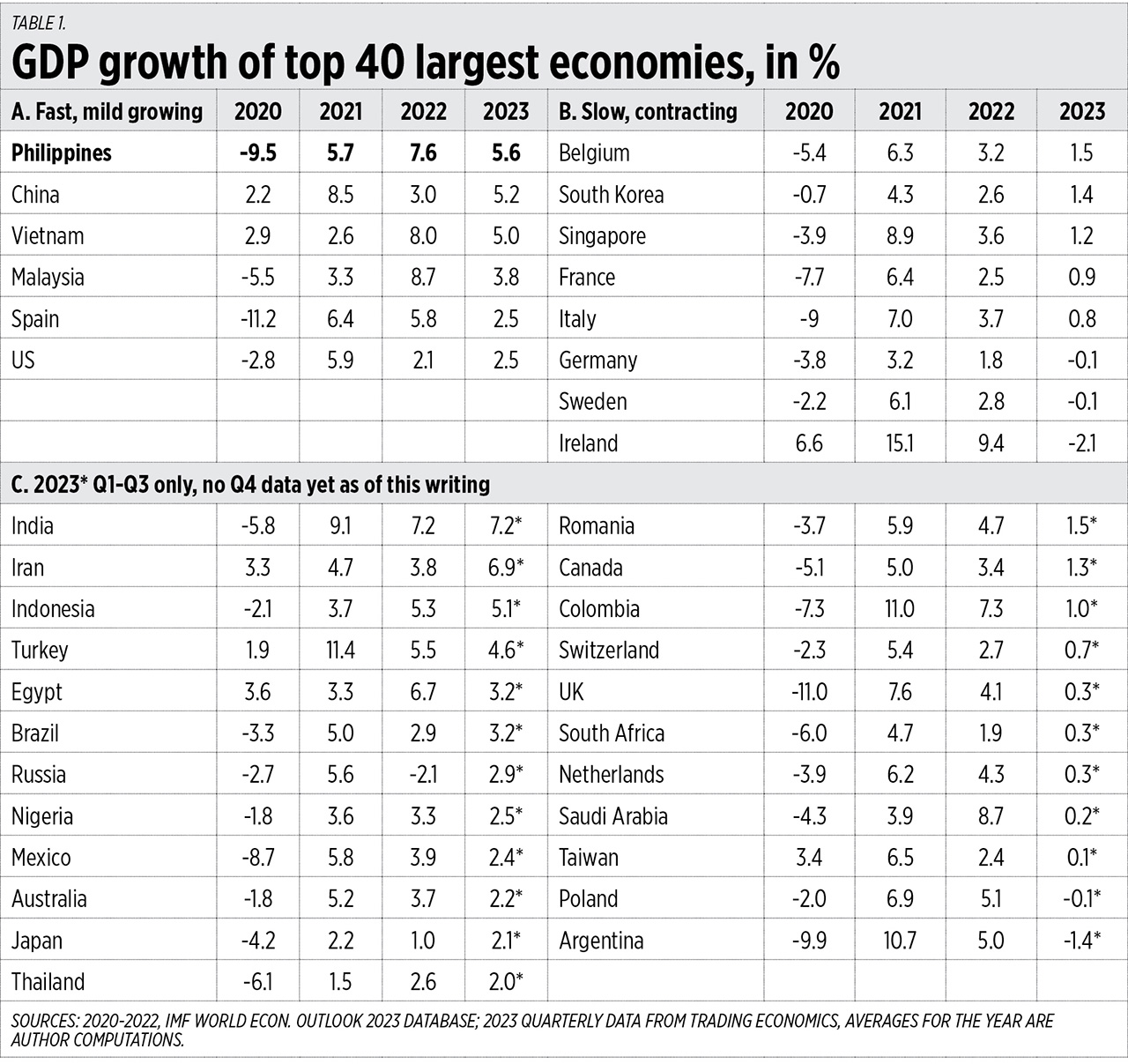

For this column, I monitored the growth of the top 40 largest economies in the world, those with GDPs of at least $700 billion in purchasing power parity (PPP) values in 2022. Two of the countries had no quarterly GDP data: Bangladesh and Pakistan. One country had data for Q1 and Q2 2023 only (for an average of 3.8%), the United Arab Emirates (UAE). So these three countries are not included among the 37 countries listed in Table 1.

{kind=link}

I grouped the countries into three. Those in Group A have full 2023 data with growth of 2.5% and above. Those in Group B grew by 2.4% and below. And those in Group C had data for Q1-Q3 2023 only, with no Q4 data available yet. The results are interesting.

1. The Philippines has the fastest growth among the countries with full 2023 data. If those in Group C are included, the Philippines had the third-fastest growth after India and Iran.

2. The Philippines’ 5.6% growth in 2023 is high growth over a high base (which was the high growth in 2022) and hence, there is no so-called “base effect.” China’s 5.2% growth in 2023 is high growth over a low base, since it had low growth of 3% in 2022.

3. The European economies, except Spain and Turkey, are either crawling at 0.1% to 1.5% growth, or are contracting (Germany, Sweden, Ireland, Poland). Other European countries not in the top 40, those ranked among the 41st to 50th largest economies, are also contracting — Austria (-0.6%), the Czech Republic (-0.5%), and Finland (-0.5%) (see Table 1).

The US growth of 2.5% seems deceptive, as it is due to heavily debt-driven government spending. The US federal debt has increased from $31 trillion in 2022 to $34 trillion in 2023, a huge $3 trillion increase in just one year. In their fiscal year 2024 budget of about $6.7 trillion, $1 trillion is earmarked for interest payments alone. Meaning their leeway for public infrastructure and social services is now drastically affected. As of Jan. 29, 2024, the US federal debt was $31.14 trillion.

HIGH GROWTH IN HOUSEHOLD SPENDING, INVESTMENTS, SERVICES SECTORSGDP is measured in two ways: by expenditure or demand side, and by industrial origin or supply side. GDP by demand is equal to GDP by supply.

In the Philippines’ GDP by demand, household consumption constitutes 73% of GDP and it grew 5.6% in 2023. Investments grew by 5.4%, but government consumption tanked at 0.4%. This is mainly due to base effect.

Budget Secretary Amenah F. Pangandaman noted that: “There were some large government spending and subsidies in Q4 2022, like high vaccine procurement and ‘Libreng Sakay’ for Metro Manila buses, that were downscaled or discontinued in Q4 2023 to help control the deficit and borrowings. That fiscal consolidation move will give us wider fiscal space this year to continue high government spending on infrastructure. Public infrastructure last year remained high but is counted in investment or capital formation where there was high growth of 11.2% in Q4.” Good decision there, Madam Secretary.

In GDP by supply, the services sector constitutes 61% of GDP and it grew by 7.2% last year. The industry sector makes up 29% of GDP and it grew at a modest 3.6% (see Table 2).

The world economy will remain in a bad shape this year, led by the US and Europe, but Asian economies will anchor modest to high growth levels, led by India, China, Indonesia, Japan, Iran, Vietnam, and the Philippines.

A debt-financed growth is unsustainable and will lead to the bubble bursting in the short to medium term. The economic team led by Finance Secretary Ralph Recto must continue to aim for sustained high growth of 6% and up, a low inflation rate, a low interest rate, and a low unemployment rate of below 4%.

Secretary Recto’s “no new taxes” plan for this year and possibly beyond is a brilliant move. Allow the households and companies to keep more of their income and savings because they will spend or invest it anyway, mostly in the domestic economy.

BIENVENIDO S. OPLAS, JR.is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.

minimalgovernment@gmail.com